BI & ReportingRevenue IntelligenceRevOpsSaaS RevOps AI Agents10 min read

Understanding SaaS financials means connecting what’s booked, billed, earned, and collected. This post maps the full ARR-to-cash lifecycle so leaders can eliminate revenue confusion and make better growth decisions.

In subscription-based models, growth and valuation depend on recurring revenue visibility — not just on what you’ve earned but also on what’s contracted, billed, collected, and recognized.

However, SaaS leaders often struggle to reconcile five critical financial components:

Each plays a unique role in bridging bookings to billings, billings to revenue, and revenue to cash flow. Understanding their connection ensures your balance sheet, income statement, and cash flow statement align perfectly.

Here’s how the complete flow works:

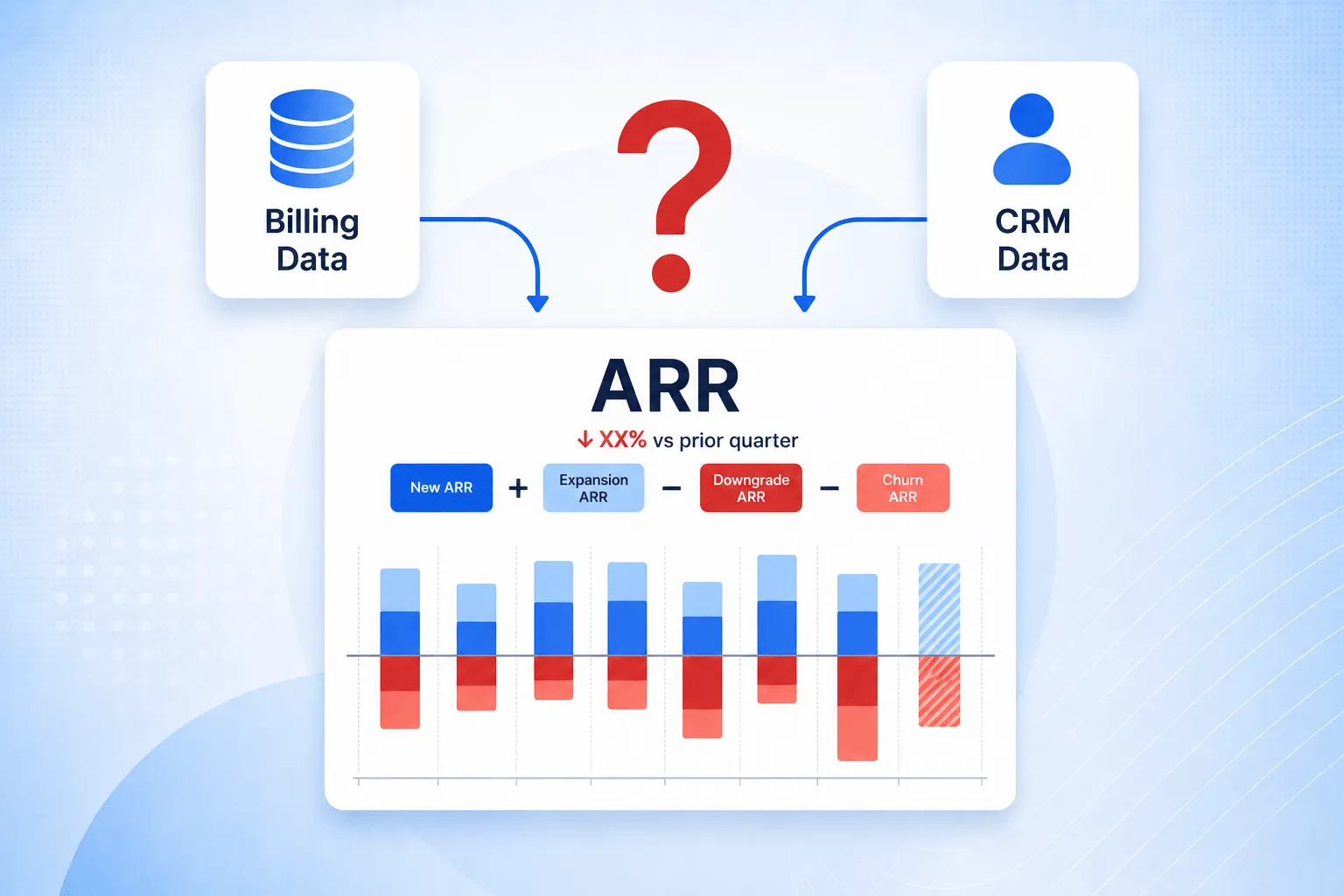

This process shows how SaaS revenue evolves from contracted value (ARR) to earned income (recognized revenue) to liquid assets (cash).

ARR represents the annualized value of active recurring contracts. It measures growth momentum and predictability.

However, ARR is non-financial — it’s not reflected on your financial statements. Instead, it informs billings, which lead to invoices.

Example:

A 12-month, $12,000 subscription = ARR of $12,000.

Billing frequency (monthly or annually) determines when it becomes invoice and revenue.

Invoices formalize the right to collect money from customers.

They can be issued before or after service delivery depending on billing policy.

Invoice Timing Matters:

Invoices are the trigger point for both Accounts Receivable and Deferred Revenue.

Once an invoice is sent, it creates Accounts Receivable (A/R) — the amount owed by a customer.

A/R sits on the balance sheet as an asset, representing revenue that’s been billed but not yet paid.

Example:

You issue a $12,000 annual invoice on Jan 1.

A/R Journal Entry Example:

If you recognize the revenue over time, that $12,000 will move from Deferred Revenue to Recognized Revenue as months pass.

Cash is recorded once payment for an invoice is received.

In SaaS, payments often occur upfront, meaning cash inflows precede revenue recognition.

This timing difference explains why cash flow and profitability can look very different in subscription businesses.

Example Flow:

Accounting Entry:

Deferred revenue represents unearned income — cash received in advance of fulfilling obligations.

It sits as a liability on the balance sheet because the company still owes service time.

Example:

A customer prepays $12,000 for a 12-month subscription in January.

→ The company recognizes $1,000 each month while $11,000 remains deferred.

This ensures compliance with ASC 606 and IFRS 15, both of which mandate recognizing revenue only when earned.

Recognized revenue reflects income from services delivered within the period.

Each month, a portion of Deferred Revenue becomes Recognized Revenue.

This structured recognition ensures accurate income reporting and aligns the income statement with the balance sheet.

ARR → Invoice → A/R → Deferred Revenue → Revenue → Cash

Below is a simplified visualization of the SaaS revenue lifecycle:

This full-cycle understanding eliminates confusion between what’s booked, billed, earned, and collected — a critical distinction for SaaS CFOs.

Practical Example: Annual Prepaid SaaS Subscription

This model shows how a single contract affects every financial statement over time.

It remains in Accounts Receivable until payment is collected or written off as bad debt.

Yes, ARR includes all active contracts, even if not invoiced or paid yet.

No. Deferred revenue is a liability (cash received in advance), while A/R is an asset (money owed by customers).

At least monthly — this ensures your revenue waterfall aligns with your general ledger.

Platforms like Discern can bring together and calculate contracts, invoices, A/R, and revenue schedules seamlessly.

To truly understand SaaS financials, you must connect the dots between:

ARR → Invoice → Accounts Receivable → Cash → Deferred Revenue → Recognized Revenue

This complete bridge provides accurate forecasting, audit-ready reporting, and trustworthy data for investors.

By mastering these relationships, SaaS CFOs and founders can make smarter growth decisions and maintain financial transparency.

Join 30+ B2B software companies and PE firms that trust Discern for automated, board-ready analytics.

Book a Demo4.8/5 100+ Reviews

Trusted by the world leaders